If you are interested in purchasing a home, how much money should you put down? This is a difficult question that all potential homeowners need to answer, as it will dictate the size and location of the house you can afford. There are a number of factors to consider, so what do you need to know?

If you are interested in purchasing a home, how much money should you put down? This is a difficult question that all potential homeowners need to answer, as it will dictate the size and location of the house you can afford. There are a number of factors to consider, so what do you need to know?

Generally, Putting More Down Is Better

There is a solid chance that a home loan is going to be the largest loan you will ever take out in your life. Therefore, there is some risk involved, and you must make sure you can pay it back. You can reduce the risk you take on by putting more money down. That way, you don’t necessarily have to take out such a large loan, and your lender may provide you with a lower interest rate. This could save you thousands of dollars over the life of the loan.

First-Time Homebuyer Options Are Available

The downside of saving up such a large down payment is that it could take a long time for you to save up so much money. Fortunately, there are programs available for first-time home buyers. For example, if you qualify for an FHA-backed loan for first-time homebuyers, you might be able to qualify for a home loan with as little as 3.5 percent down. This might make it easier for you to afford a house.

Is Your Money Better Served In The Market?

Putting more money down for a house may provide you with a lower interest rate while also reducing your monthly mortgage payments; however, you need to think about where your money will work the hardest for you. You may qualify for a lower interest rate if you put more money down, but will your money generate a higher return if you invested in your retirement? You should answer this question when you decide whether to put more money towards your house or more money in an investment portfolio.

Consider Working With An Expert

How much money should you put down for your house? This is a question that has a different answer for everyone, which is why you should consider working with a professional who can help you.

There are many complicated terms thrown around regarding your mortgage, and one of them is an escrow account. You will probably hear that your lender will collect some additional money every month for escrow payments. If you take a look at your mortgage statement, you will see your interest, your principal, and your escrow. What does this mean, and why do you have to pay additional money that isn’t going toward the balance of your loan?

There are many complicated terms thrown around regarding your mortgage, and one of them is an escrow account. You will probably hear that your lender will collect some additional money every month for escrow payments. If you take a look at your mortgage statement, you will see your interest, your principal, and your escrow. What does this mean, and why do you have to pay additional money that isn’t going toward the balance of your loan? There are many people who dream of owning a home, but you need to purchase your home for the right reasons. Simply purchasing a house because other people are doing so is not a strong reason to make such an expensive purchase. What are some of the reasons why you should purchase a house? What are some examples of bad reasons to buy a home?

There are many people who dream of owning a home, but you need to purchase your home for the right reasons. Simply purchasing a house because other people are doing so is not a strong reason to make such an expensive purchase. What are some of the reasons why you should purchase a house? What are some examples of bad reasons to buy a home? What do you need to do if you want to improve the safety and functionality of your home? You may not think that your home has a lot of safety hazards, but you might be surprised at how many people get hurt at home every year. Particularly if you have older people in your home, or if you have people in your house with disabilities, you need to pay close attention to your safety and functionality. What are a few tips you should keep in mind?

What do you need to do if you want to improve the safety and functionality of your home? You may not think that your home has a lot of safety hazards, but you might be surprised at how many people get hurt at home every year. Particularly if you have older people in your home, or if you have people in your house with disabilities, you need to pay close attention to your safety and functionality. What are a few tips you should keep in mind?  As you get closer to your retirement age, you should try to discharge as much of your debt as possible. Unfortunately, many people close to the age of retirement still have a significant mortgage balance they need to pay off. What are some of the top reasons why you should pay off your mortgage before you retire?

As you get closer to your retirement age, you should try to discharge as much of your debt as possible. Unfortunately, many people close to the age of retirement still have a significant mortgage balance they need to pay off. What are some of the top reasons why you should pay off your mortgage before you retire? If you own a home, you will see a lot of information about your payment schedule. It specifies exactly what payments you have to make, when you have to make them, and how much of each payment will go toward your principal and interest. This is called an amortization schedule, and it is typically designed in such a way that your last payment pays off your loan down to the penny. How does this impact the life of your loan?

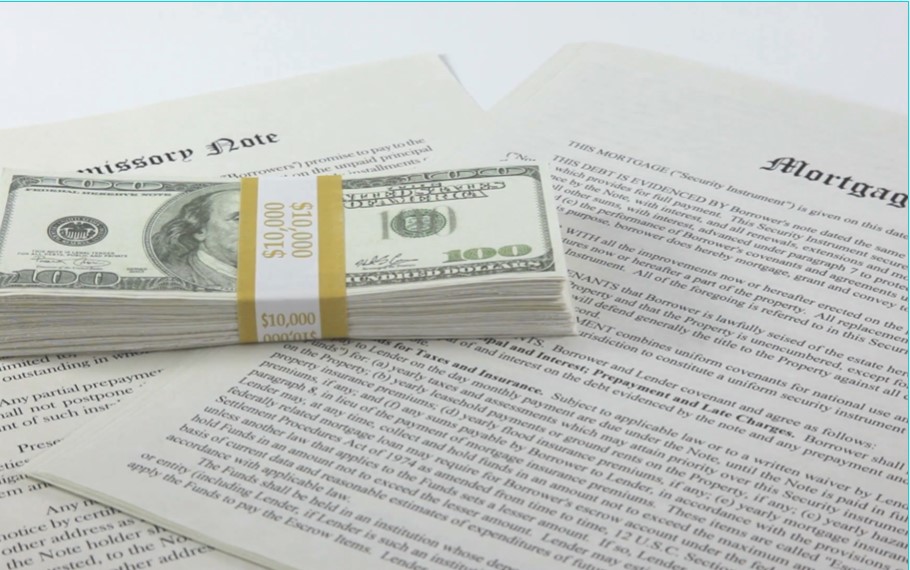

If you own a home, you will see a lot of information about your payment schedule. It specifies exactly what payments you have to make, when you have to make them, and how much of each payment will go toward your principal and interest. This is called an amortization schedule, and it is typically designed in such a way that your last payment pays off your loan down to the penny. How does this impact the life of your loan? There are some people who are able to pay cash for a home. Typically, these are individuals who are selling an existing property that has gone up in value. Now, all of a sudden, they have a lot of extra money they can spend on a house. If you can pay cash for a home, you have a lot of extra negotiating power. When it is time to complete the sale, who pays?

There are some people who are able to pay cash for a home. Typically, these are individuals who are selling an existing property that has gone up in value. Now, all of a sudden, they have a lot of extra money they can spend on a house. If you can pay cash for a home, you have a lot of extra negotiating power. When it is time to complete the sale, who pays? If you are interested in purchasing a house, you need to review all of the offers available. The vast majority of loan officers are going to talk about something called qualifying mortgages, which is usually shortened to QM. You may be asking, what is a non-qualifying mortgage? This is usually shortened to Non-QM, and it simply means that the loan does not conform with the rules and regulations put in place by the Consumer Financial Protection Bureau, usually shortened to CFPB. What are the differences between a QM and Non-QM mortgage, and which one is right for your needs?

If you are interested in purchasing a house, you need to review all of the offers available. The vast majority of loan officers are going to talk about something called qualifying mortgages, which is usually shortened to QM. You may be asking, what is a non-qualifying mortgage? This is usually shortened to Non-QM, and it simply means that the loan does not conform with the rules and regulations put in place by the Consumer Financial Protection Bureau, usually shortened to CFPB. What are the differences between a QM and Non-QM mortgage, and which one is right for your needs? If you are purchasing a house for the first time, you are probably excited to imagine what your life might look like in a bunch of different houses. At the same time, the process can be a bit overwhelming. The housing market is competitive right now, the financing process can be confusing, and you might not know exactly what you are looking for. What are a few of the most important tips first-time home buyers need to know?

If you are purchasing a house for the first time, you are probably excited to imagine what your life might look like in a bunch of different houses. At the same time, the process can be a bit overwhelming. The housing market is competitive right now, the financing process can be confusing, and you might not know exactly what you are looking for. What are a few of the most important tips first-time home buyers need to know? The housing market today is very competitive, and you might be wondering how you can get your offer accepted. If the seller has multiple offers on the table, it can be a bit of a challenge. Many people assume that the best way to get an offer accepted is to offer the most money. Even though that is certainly helpful, there are several other tips you should follow to make sure your offer is the one the seller picks.

The housing market today is very competitive, and you might be wondering how you can get your offer accepted. If the seller has multiple offers on the table, it can be a bit of a challenge. Many people assume that the best way to get an offer accepted is to offer the most money. Even though that is certainly helpful, there are several other tips you should follow to make sure your offer is the one the seller picks.