Buying a home, a car, or any significant investment often involves making a down payment. The down payment is a crucial part of the purchasing process, as it can impact your loan terms, interest rates, and monthly payments. But how much should you save for a down payment, and why is it so important?

Buying a home, a car, or any significant investment often involves making a down payment. The down payment is a crucial part of the purchasing process, as it can impact your loan terms, interest rates, and monthly payments. But how much should you save for a down payment, and why is it so important?

Understanding Down Payments

A down payment is a portion of the purchase price that you pay upfront when buying a house, a car, or making a large investment. It’s a way to demonstrate your commitment to the purchase and reduce the risk for the lender or seller. Down payments are commonly associated with:

Homebuying: When purchasing a home, a down payment is typically required by mortgage lenders. The amount can vary but is often around 20% of the home’s purchase price.

Car purchases: Down payments for cars can also range, but they often hover around 10-20% of the vehicle’s price.

Large investments: In other scenarios, such as starting a business or investing in a big-ticket item, a down payment may be necessary to secure financing.

Importance of Down Payments

Lowering Monthly Payments: A larger down payment reduces the amount you need to finance, resulting in lower monthly payments. This can make your financial burden more manageable in the long run.

Qualifying for Loans: A substantial down payment can help you qualify for loans with more favorable terms and lower interest rates. Lenders often see a larger down payment as a sign of financial stability.

Building Equity: With a significant down payment, you’ll start building equity in your asset from day one. Equity is the portion of the property or asset you own, and it can grow over time, giving you more financial security.

How Much Should You Save for a Down Payment?

The ideal down payment amount can vary based on what you’re buying and your financial situation. Here are some general guidelines:

Homes: As mentioned earlier, a down payment of 20% is often recommended for purchasing a home. However, there are mortgage options that allow for lower down payments, such as FHA loans, which require as little as 3.5% down. The key is to balance a lower down payment with the added cost of private mortgage insurance (PMI) and potentially higher interest rates.

Cars: For buying a car, a down payment of 10-20% is a good range to aim for. This will help reduce the overall cost of the car loan and lower your monthly payments.

Large Investments: The down payment for investments can vary widely, so it’s essential to assess your specific financial goals and risks. In this case, consult with a financial advisor to determine the right amount.

How to Save for a Down Payment

Saving for a down payment may seem daunting, but with a clear plan, it’s achievable. Here are some steps to help you get started:

Create a Budget: Review your finances, set a budget, and identify areas where you can cut back on spending to save more.

Open a Dedicated Savings Account: Consider opening a separate savings account exclusively for your down payment fund. This will help you track your progress and keep the money out of sight and out of mind.

Automate Savings: Set up automatic transfers from your checking account to your down payment savings account. This ensures that you save consistently.

Increase Income: Explore opportunities to increase your income, such as taking on a part-time job or freelancing, to boost your savings rate.

Reduce Debt: Pay down high-interest debts like credit cards to free up more money for saving.

The role of down payments in major purchases cannot be overstated. They play a vital role in reducing the financial burden of loans, helping you secure better loan terms, and building equity in your assets. While the ideal down payment amount can vary, it’s essential to set a clear savings goal and follow a strategic plan to achieve it. With discipline and patience, you can save for a down payment and take a significant step toward achieving your financial goals.

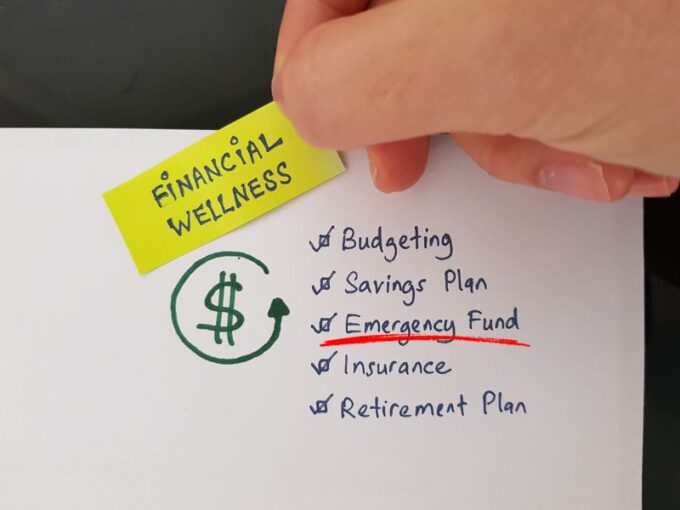

It’s important to be financially prepared for emergencies so that you can handle unexpected expenses or situations without having to worry about your financial stability. Here are some ways to financially prepare for emergencies:

It’s important to be financially prepared for emergencies so that you can handle unexpected expenses or situations without having to worry about your financial stability. Here are some ways to financially prepare for emergencies: The holiday season is a time of joy and celebration, but it can also be a challenging time for your finances, especially if you’re juggling the responsibilities of a mortgage. However, with some thoughtful planning and budgeting, you can ensure that you enjoy the festivities without putting your financial stability at risk. I will provide you with essential tips and strategies to help you manage your mortgage budget during the holiday season.

The holiday season is a time of joy and celebration, but it can also be a challenging time for your finances, especially if you’re juggling the responsibilities of a mortgage. However, with some thoughtful planning and budgeting, you can ensure that you enjoy the festivities without putting your financial stability at risk. I will provide you with essential tips and strategies to help you manage your mortgage budget during the holiday season. When someone is looking at purchasing a home, they usually focus on the purchase price of the home and the potential monthly payment. At the same time, there are other costs that need to be included as well. This includes home insurance and real estate taxes.

When someone is looking at purchasing a home, they usually focus on the purchase price of the home and the potential monthly payment. At the same time, there are other costs that need to be included as well. This includes home insurance and real estate taxes.

If you are planning on purchasing a home in the near future, you need to make sure you have enough money saved up. While there are a lot of expenses that go along with purchasing a home, the biggest expense is the down payment.

If you are planning on purchasing a home in the near future, you need to make sure you have enough money saved up. While there are a lot of expenses that go along with purchasing a home, the biggest expense is the down payment. Right now, mortgage rates have fallen to rates that haven’t been seen in years. This opens the door for many people to apply for a mortgage that they previously may not have been able to afford. Sadly, not everyone who applies for a mortgage is going to be approved. There are a few steps that applicants can take to increase their chances of getting their mortgage application approved.

Right now, mortgage rates have fallen to rates that haven’t been seen in years. This opens the door for many people to apply for a mortgage that they previously may not have been able to afford. Sadly, not everyone who applies for a mortgage is going to be approved. There are a few steps that applicants can take to increase their chances of getting their mortgage application approved. For those who are looking to buy a home, they know that this is one of the most exciting experiences in the world. There is something special that comes with looking at a bunch of homes and envisioning a life there.

For those who are looking to buy a home, they know that this is one of the most exciting experiences in the world. There is something special that comes with looking at a bunch of homes and envisioning a life there. By now, it should be apparent that this COVID-19 (Corona-virus) pandemic is going to be here for several months. It is already causing the market to plummet and is disrupting jobs all over the country. Many people who work as hourly employees (or are independent contractors) are starting to suffer. As people’s budgets start to feel the squeeze, this is exactly the time that people should be relying on an emergency fund; however, for those who don’t have one, it is time to start saving.

By now, it should be apparent that this COVID-19 (Corona-virus) pandemic is going to be here for several months. It is already causing the market to plummet and is disrupting jobs all over the country. Many people who work as hourly employees (or are independent contractors) are starting to suffer. As people’s budgets start to feel the squeeze, this is exactly the time that people should be relying on an emergency fund; however, for those who don’t have one, it is time to start saving. Those who are looking at buying a home need to think about whether or not they are truly ready for this responsibility. When someone takes out a mortgage, this is frequently the largest loan someone will ever apply for in their life. Furthermore, owning a home also means homeowners insurance, real estate taxes, home maintenance, and home repairs.

Those who are looking at buying a home need to think about whether or not they are truly ready for this responsibility. When someone takes out a mortgage, this is frequently the largest loan someone will ever apply for in their life. Furthermore, owning a home also means homeowners insurance, real estate taxes, home maintenance, and home repairs.