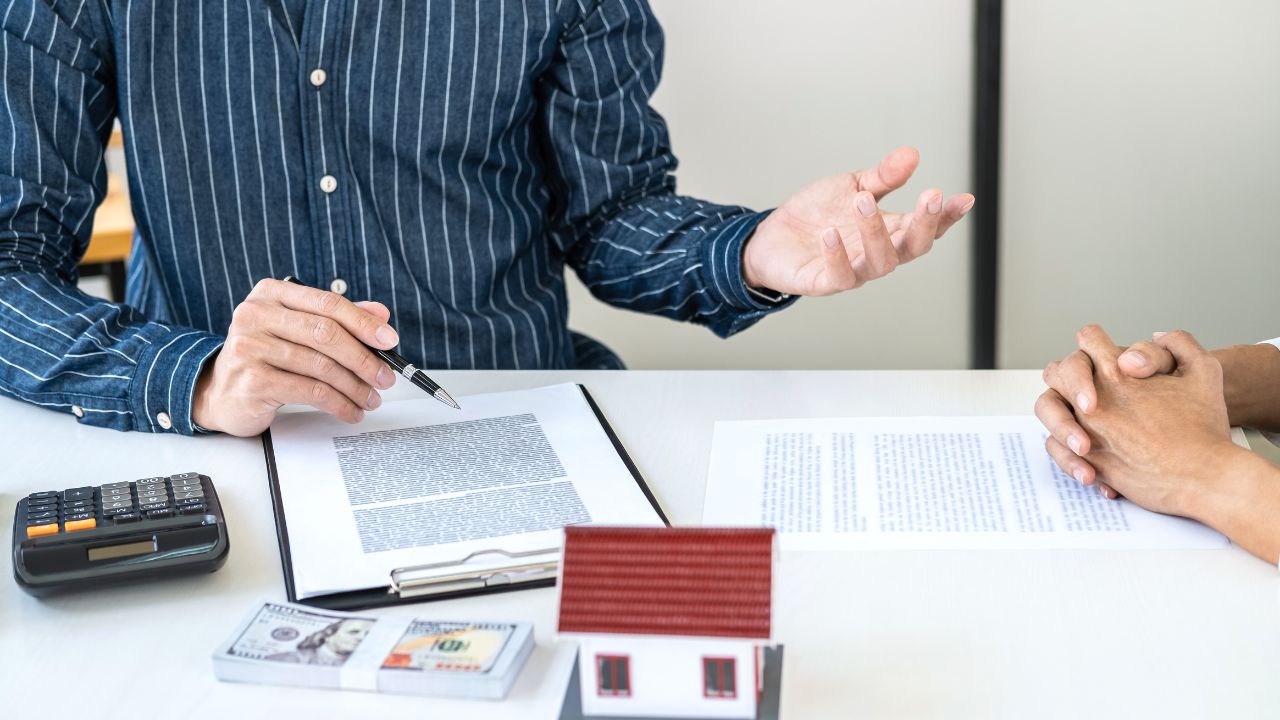

One of the biggest questions future homeowners ask is, “How much do I actually need to save before buying a home?” The answer depends on a few key components, but don’t worry—it’s easier to break down than you might think! Here’s an overview of what you need to save to step into homeownership confidently.

One of the biggest questions future homeowners ask is, “How much do I actually need to save before buying a home?” The answer depends on a few key components, but don’t worry—it’s easier to break down than you might think! Here’s an overview of what you need to save to step into homeownership confidently.

1. The Down Payment

The down payment is the first major cost to consider. The traditional 20% down payment isn’t your only option anymore. Many loan programs allow buyers to get started with as little as 3% down.

For example, if you’re looking at purchasing a home priced at $350,000, a 3% down payment would be $10,500. This lower requirement opens the door to homeownership for many buyers.

If you qualify for VA or USDA loans, you may not need to pay a down payment at all. However, keep in mind that a smaller down payment might mean additional costs, such as mortgage insurance, to protect the lender.

2. Closing Costs

Next, you’ll need to factor in closing costs, which cover a variety of fees associated with finalizing your home purchase. These typically range from 2% to 5% of the home’s price and include expenses like:

-

Loan origination fees

-

Title insurance

-

Home appraisal and inspection

-

Prepaid property taxes and insurance

On a $350,000 home, closing costs at 3% would add $10,500 to your upfront expenses. However, some lenders and sellers offer incentives or credits to help cover these costs, so it’s worth asking about these options during the process.

3. Emergency Fund

An emergency fund is a critical part of your financial preparation. Owning a home brings new responsibilities, and unexpected expenses—like a leaky roof or a broken appliance—can arise.

Experts recommend having at least three to six months of living expenses saved as a safety net. If your monthly mortgage payment is around $2,200, you should aim for at least $6,600 to $13,200 in your emergency fund. This provides peace of mind and ensures you won’t find yourself in a financial bind after moving in.

The Grand Total

Let’s put it all together. Here’s a rough estimate of what you’ll need:

-

Down Payment (3%): $10,500

-

Closing Costs (3%): $10,500

-

Emergency Fund (3 months): $6,600

Grand Total: At least $27,600 to comfortably buy a $350,000 home.

Remember, these numbers will vary based on the home price, type of loan, and any financial assistance programs you might qualify for. Some buyers may be able to save less, while others might choose to save more for added security.

Tips to Get Started

-

Set a Savings Goal: Break down your total into monthly savings targets to stay on track.

-

Explore Assistance Programs: Look into grants, down payment assistance, or first-time buyer programs in your area.

-

Work with a Professional: A knowledgeable real estate agent or lender can help you navigate financing options and understand the true costs of homeownership.

If buying a home is on your horizon, now is the perfect time to start saving and planning. Whether you’re just getting started or ready to make a move, I’m here to guide you every step of the way. Let’s create a savings plan that works for your budget and timeline so you can step into homeownership with confidence.

As remote work becomes a standard part of life, the traditional home office is undergoing a major transformation. What was once a corner desk or spare room has now evolved into a personalized, stylish, and functional space. Homeowners are getting creative, designing offices that not only cater to their work needs but also reflect their unique personalities and styles.

As remote work becomes a standard part of life, the traditional home office is undergoing a major transformation. What was once a corner desk or spare room has now evolved into a personalized, stylish, and functional space. Homeowners are getting creative, designing offices that not only cater to their work needs but also reflect their unique personalities and styles.

Selling your home can be exciting and emotional. You may be focused on the potential profit from the sale, it’s essential to understand the costs that come with closing the deal. Closing costs can significantly impact your net proceeds, so being prepared will help you avoid surprises and plan accordingly.

Selling your home can be exciting and emotional. You may be focused on the potential profit from the sale, it’s essential to understand the costs that come with closing the deal. Closing costs can significantly impact your net proceeds, so being prepared will help you avoid surprises and plan accordingly.  When selling your home, first impressions are everything. A clean, well-organized space allows potential buyers to envision themselves living there and can even increase the perceived value of your property. Cleaning is not just about making your home look good; it’s a strategic move to ensure your home stands out in a competitive market. Here’s how to tackle the cleaning process effectively when preparing your home for sale.

When selling your home, first impressions are everything. A clean, well-organized space allows potential buyers to envision themselves living there and can even increase the perceived value of your property. Cleaning is not just about making your home look good; it’s a strategic move to ensure your home stands out in a competitive market. Here’s how to tackle the cleaning process effectively when preparing your home for sale. Finding your dream home is one of the most exciting and personal journeys you’ll ever take. Just like crafting the perfect cup of coffee, choosing the right home is all about finding the blend that matches your unique preferences. For some, it’s all about practicality, while for others, it’s about charm, savings, or convenience.

Finding your dream home is one of the most exciting and personal journeys you’ll ever take. Just like crafting the perfect cup of coffee, choosing the right home is all about finding the blend that matches your unique preferences. For some, it’s all about practicality, while for others, it’s about charm, savings, or convenience. When most people think about buying a home, the spring and summer months often come to mind. After all, that’s when the market is buzzing with activity. However, what many don’t realize is that January can be one of the best times to purchase a home. From motivated sellers to financial benefits, buying during the winter months offers several unique advantages for savvy homebuyers.

When most people think about buying a home, the spring and summer months often come to mind. After all, that’s when the market is buzzing with activity. However, what many don’t realize is that January can be one of the best times to purchase a home. From motivated sellers to financial benefits, buying during the winter months offers several unique advantages for savvy homebuyers.

When it comes to real estate, you’ve likely heard the phrase, “Location, location, location!” This isn’t just a catchy mantra, it’s a fundamental truth that underscores the value of any property. While a home’s design, size, and features play a role in your buying decision, the location is often the most critical factor that determines both the property’s current worth and its long-term potential.

When it comes to real estate, you’ve likely heard the phrase, “Location, location, location!” This isn’t just a catchy mantra, it’s a fundamental truth that underscores the value of any property. While a home’s design, size, and features play a role in your buying decision, the location is often the most critical factor that determines both the property’s current worth and its long-term potential. As we step into 2025, it’s the perfect time to reflect on the possibilities a new year can bring, especially when it comes to your real estate goals. Whether you’re dreaming of buying your first home, investing in property, or upgrading your current living space, setting clear, actionable resolutions can help guide your journey and turn your aspirations into reality.

As we step into 2025, it’s the perfect time to reflect on the possibilities a new year can bring, especially when it comes to your real estate goals. Whether you’re dreaming of buying your first home, investing in property, or upgrading your current living space, setting clear, actionable resolutions can help guide your journey and turn your aspirations into reality.