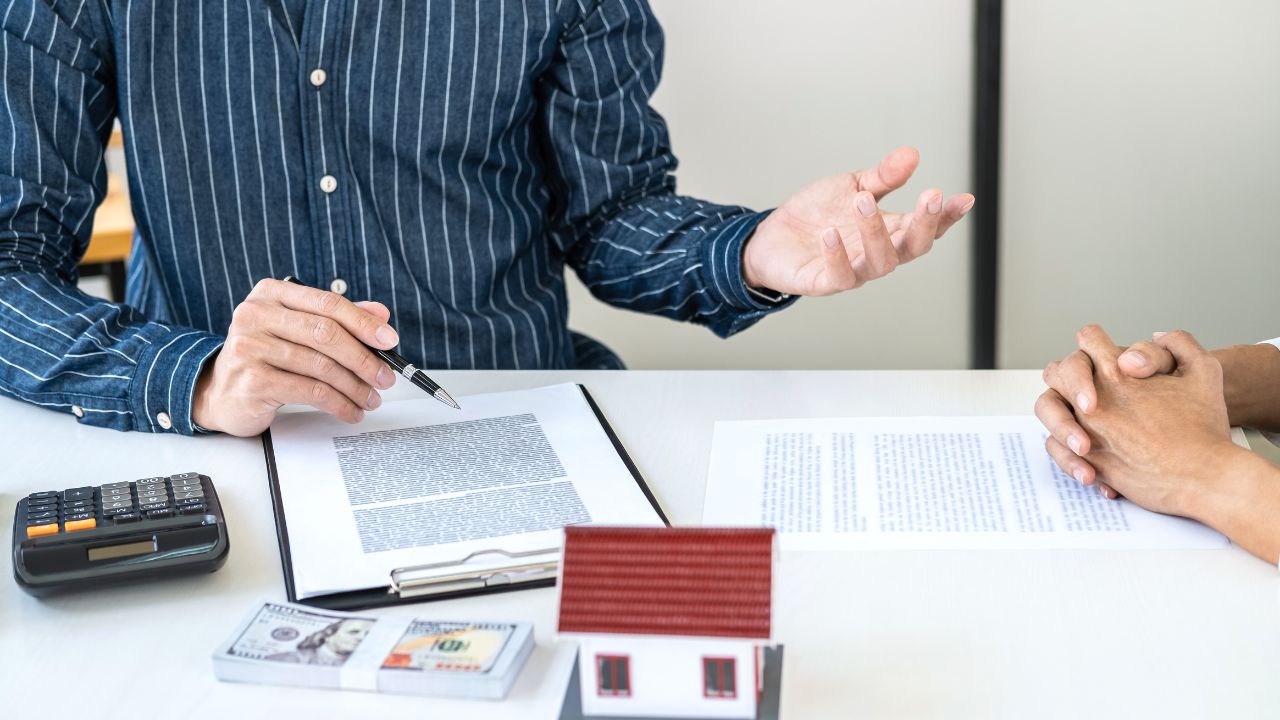

When buying or selling a home, you’ll likely encounter both a home inspection and a home appraisal. While these processes are essential for ensuring a smooth real estate transaction, they serve different purposes and involve unique evaluations. Understanding the differences between a home inspection and a home appraisal can help you navigate the home-buying or selling process more confidently.

When buying or selling a home, you’ll likely encounter both a home inspection and a home appraisal. While these processes are essential for ensuring a smooth real estate transaction, they serve different purposes and involve unique evaluations. Understanding the differences between a home inspection and a home appraisal can help you navigate the home-buying or selling process more confidently.

What Is a Home Inspection?

A home inspection is an in-depth evaluation of a property’s condition. It is typically ordered by the buyer and conducted by a licensed home inspector. The goal is to identify any current or potential issues with the property that could affect its safety, functionality, or value.

What Does It Include?

A home inspector examines various aspects of the home, including:

-

Structural elements (foundation, walls, roof)

-

Electrical systems

-

Plumbing systems

-

HVAC systems (heating, ventilation, and air conditioning)

-

Appliances

-

Interior and exterior features

The inspector provides a detailed report of their findings, which the buyer can use to negotiate repairs, request credits, or reconsider the purchase.

Who Benefits?

The primary beneficiary of a home inspection is the buyer. It provides a clear understanding of the property’s condition, helping them make an informed decision.

What Is a Home Appraisal?

A home appraisal is an evaluation of a property’s market value, typically ordered by the buyer’s lender. It is conducted by a licensed appraiser who assesses the property’s worth based on factors like its size, location, condition, and comparable sales in the area.

What Does It Include?

An appraisal focuses more on value than condition. The appraiser will:

-

Assess the property’s overall condition and curb appeal.

-

Compare it to recently sold homes in the area with similar features (comparables or “comps”).

-

Factor in local real estate trends.

The appraiser’s report determines the home’s fair market value, which the lender uses to ensure the loan amount is appropriate for the property’s worth.

Who Benefits?

The primary beneficiary of a home appraisal is the lender. It protects their investment by ensuring the home is worth the loan amount. Buyers also benefit by confirming that they are not overpaying for the property.

Key Differences:

Home Inspection

Purpose: To evaluate property condition

Ordered By: Buyer

Conducted By: Licensed home inspector

Focus: Structural integrity, safety, and repairs

Who Benefits? Buyer

Home Appraisal

Purpose: To determine property market value

Ordered By: Lender

Conducted By: Licensed home appraiser

Focus: Market value and comparable properties

Who Benefits? Lender and buyer

Why Both Are Important

Both a home inspection and a home appraisal play crucial roles in the real estate process:

-

For Buyers: A home inspection ensures the property is in good condition, while an appraisal ensures the price is fair.

-

For Sellers: Addressing inspection issues in advance can make the home more attractive to buyers. An appraisal helps set a realistic price for the market.

-

For Lenders: An appraisal ensures the loan amount matches the property’s value, reducing financial risk.

Understanding the difference between a home inspection and a home appraisal is key to navigating the home-buying or selling journey. Both processes provide essential information, but they serve distinct purposes. A home inspection ensures you’re aware of any potential issues, while a home appraisal confirms you’re paying (or receiving) a fair price for the property.

By being informed and prepared, you can ensure a smoother transaction and greater peace of mind in one of life’s most significant investments.

The journey to purchasing or selling a home can be a thrilling experience, but it also involves a series of legal steps that need to be clearly understood. The real estate legal process includes contracts, disclosures, and closing procedures, all of which are essential for ensuring that both buyers and sellers are protected throughout the transaction. In this post, we will break down these key terms so you can be prepared and informed during your home-buying or selling journey.

The journey to purchasing or selling a home can be a thrilling experience, but it also involves a series of legal steps that need to be clearly understood. The real estate legal process includes contracts, disclosures, and closing procedures, all of which are essential for ensuring that both buyers and sellers are protected throughout the transaction. In this post, we will break down these key terms so you can be prepared and informed during your home-buying or selling journey. Finding your dream home is one of the most exciting and personal journeys you’ll ever take. Just like crafting the perfect cup of coffee, choosing the right home is all about finding the blend that matches your unique preferences. For some, it’s all about practicality, while for others, it’s about charm, savings, or convenience.

Finding your dream home is one of the most exciting and personal journeys you’ll ever take. Just like crafting the perfect cup of coffee, choosing the right home is all about finding the blend that matches your unique preferences. For some, it’s all about practicality, while for others, it’s about charm, savings, or convenience. If you’re in the market to buy a duplex or similar multi-unit property, you may be wondering whether you can use an FHA loan to finance your purchase. FHA loans are well-known for helping first-time homebuyers, but they can also be used to purchase duplexes. Here’s everything you need to know about FHA loans, how they work, and whether they’re a good fit for your homebuying plans.

If you’re in the market to buy a duplex or similar multi-unit property, you may be wondering whether you can use an FHA loan to finance your purchase. FHA loans are well-known for helping first-time homebuyers, but they can also be used to purchase duplexes. Here’s everything you need to know about FHA loans, how they work, and whether they’re a good fit for your homebuying plans. As remote work continues to progress, having a well-designed home office is more than just a luxury, it has become a necessity. A thoughtfully created workspace can increase productivity, boost creativity, and promote overall well-being. I have seen how creating a productive environment impacts work-from-home efficiency and comfort. Whether you’re setting up a corner nook or dedicating an entire room, here are six practical ideas to transform your home office into an ideal place to get things done.

As remote work continues to progress, having a well-designed home office is more than just a luxury, it has become a necessity. A thoughtfully created workspace can increase productivity, boost creativity, and promote overall well-being. I have seen how creating a productive environment impacts work-from-home efficiency and comfort. Whether you’re setting up a corner nook or dedicating an entire room, here are six practical ideas to transform your home office into an ideal place to get things done. When it comes to homeownership, one of the most important aspects of the process is ensuring you have the proper legal documentation that proves your ownership. This documentation usually comes in the form of a title or a deed. These documents not only provide proof of ownership but also serve as a way to protect your rights to the property. Whether you’re buying your first home or adding to your real estate portfolio, understanding the difference between titles and deeds is essential to securing your investment.

When it comes to homeownership, one of the most important aspects of the process is ensuring you have the proper legal documentation that proves your ownership. This documentation usually comes in the form of a title or a deed. These documents not only provide proof of ownership but also serve as a way to protect your rights to the property. Whether you’re buying your first home or adding to your real estate portfolio, understanding the difference between titles and deeds is essential to securing your investment. When preparing to sell, many homeowners consider renovations to boost their property’s appeal and value. While updating a home can make it more attractive to buyers, it’s crucial to weigh the potential benefits against the costs. Here’s a look at the pros and cons of renovating before listing to help you make an informed decision.

When preparing to sell, many homeowners consider renovations to boost their property’s appeal and value. While updating a home can make it more attractive to buyers, it’s crucial to weigh the potential benefits against the costs. Here’s a look at the pros and cons of renovating before listing to help you make an informed decision. As the leaves turn and the air gets crisp, many of us start thinking about renovations that can make our homes more appealing—especially with Halloween right around the corner! Whether you’re preparing for spooky festivities or planning a future sale, the right renovations can turn your home into a valuable gem. Let’s dive into some hauntingly good renovations that can raise your home’s value without leaving you in a fright!

As the leaves turn and the air gets crisp, many of us start thinking about renovations that can make our homes more appealing—especially with Halloween right around the corner! Whether you’re preparing for spooky festivities or planning a future sale, the right renovations can turn your home into a valuable gem. Let’s dive into some hauntingly good renovations that can raise your home’s value without leaving you in a fright!

When you’re searching for a home, knowing the state of the local market is essential. Whether it’s a buyer’s or seller’s market can influence everything from price negotiations to how quickly homes sell. So, how can you tell if your dream neighborhood is favoring buyers? Here are some useful tips to help you gauge the market:

When you’re searching for a home, knowing the state of the local market is essential. Whether it’s a buyer’s or seller’s market can influence everything from price negotiations to how quickly homes sell. So, how can you tell if your dream neighborhood is favoring buyers? Here are some useful tips to help you gauge the market: